How & When Do I Enroll in Medicare Parts A & B?

Within 3-6 months of turning 65, you should receive a large envelope from the Social Security Administration with information about your Medicare Part A & Part B coverage. Within this envelope, you’ll find a thicker sheet of paper which includes your Medicare ID card on one corner of the page. It has perforated edges to allow you to detach it from the page. It is thick stock paper and is your permanent ID. You will not receive a plastic ID card.

If you worked at least 40 quarters in the United States, you should automatically be enrolled in Medicare Part A (Hospital) insurance. Your card should reflect your Medicare Part A start date as the 1st of the month in which you turn 65. If you were born on the first of the month, the start date will be the first of the month prior to your birthday.

Medicare Part B (Outpatient) insurance is elective coverage. Over 90% of Medicare beneficiaries opt to take Part B. It makes sense to enroll in Part B if you would like to have coverage for medical services received outside of a hospital setting and you do not have other creditable coverage.

It’s important to note that if you do not have other creditable coverage (Employer/Group Insurance) and you wait to enroll in Part B, you could be assessed a 10% penalty for every 12-month period that you were eligible for Part B but did not sign up.

**************************************************************************************

If you are already enrolled in and are receiving Social Security income benefits prior to turning 65, you should automatically be enrolled in Medicare Part B and your card should reflect this. If you want to stay enrolled in Medicare Part A & B and your card reflects a start date for both, you do not have to do anything else other than consider a Medicare supplement plan and a Medicare Part D drug plan.

If you decide you do not want Medicare Part B, you should also have instructions to send the ID card back to opt out. If you send the card back, you will receive a new ID card within a few weeks reflecting that you are enrolled in Medicare Part A only.

Keep in mind that if you have no creditable medical coverage (not counting Medicare Part A) and opt out of Medicare Part B, you will have financial penalties (discussed later in this guide) if you decide to pick up Part B at a later time.

One of the common reasons one might return their card and opt out of Medicare Part B is if they are currently employed and have creditable health coverage through their employer. If you intend to stay employed and keep employer coverage, check with your HR department to ensure you have creditable health coverage before you opt out of Medicare Part B.

If you have not begun receiving Social Security benefits prior to turning 65, you will likely have to enroll in Medicare Part B proactively. The reason is that receiving Social Security benefits provides Medicare with a source of income from which they can deduct your Medicare Part B premium.

If you are not receiving Social Security income, you’ll want to enroll in Medicare Part B within three months prior to the month in which you turn 65. You also have the month in which you turn 65 and the three months following to enroll in Medicare Part B without penalty (unless you have creditable health coverage elsewhere). So, you have a seven-month window to enroll in Medicare Part B.

There are 3 options for enrolling in Medicare Part B if not automatically enrolled:

Online at www.ssa.gov/.

By calling Social Security at 1-800-772-1213 (TTY users 1-800-0778), Monday through Friday.

In-person at your local Social Security office. You can find your closest office by visiting the following page and entering your zip code: https://secure.ssa.gov/ICON/main.jsp.

If you haven’t started receiving Social Security benefits, you must also make monthly payments. You’ll get a monthly bill called a “Notice of Medicare Premium Payment Due.” There are 4 ways you can pay your Medicare Part B premium:

Pay directly from your bank account using your bank’s online bill payment system.

Sign up for Medicare Easy Pay, a free service that automatically deducts premium payments from your bank account each month, usually on the 20th of the month.

Mail your Medicare payment coupon and payment to: Medicare Premium Collection Center P.O. Box 790355 St. Louis, MO 63179-0355

Pay by credit card or debit card. Complete the bottom portion of the payment coupon on your Medicare bill, and sign it. You’ll need to provide the account information as it appears on your card and the expiration date. Most credit cards today only have the month and year in the expiration date field. If your credit card only has a month and year in the expiration date, fill in the month and year on the payment coupon and leave the day field blank. Mail your payment to the address above.

If you have questions regarding your Medicare eligibility or application, please call medigapHelper at (480)508-4112

What Does Medicare Part A Cover?

Medicare Part A is your hospitalization coverage. So, at a high level, Medicare Part A covers your stay in a medical facility and the associated services while in that facility. It covers services such as:

Inpatient care in hospitals

Inpatient rehabilitation facilities

Long-term care hospitals

Skilled nursing facilities

Home health care services

Hospice care

You can search whether a medical service is covered by Medicare by visiting the following page: www.medicare.gov/coverage.

While Medicare Part A covers the majority of your medical expenses while in a medical facility, you will still be required to cover deductibles and coinsurance while in the hospital (unless you own a Medicare supplement plan that covers them).

You will have a responsibility to cover the following (in 2025):

HOSPITAL STAY

$1,676 deductible for each benefit period

Days 1-60: $0 coinsurance for each benefit period

Days 61-90: $419 coinsurance per day of each benefit period

Days 91 and beyond: $838 coinsurance per each “lifetime reserve day” after day 90 for each benefit period (up to 60 days over your lifetime)

Beyond lifetime reserve days: all costs

SKILLED NURSING FACILITY STAY

$0 for the first 20 days of each benefit period

$209.50 per day for days 21–100 of each benefit period

All costs for each day after day 100 of the benefit period

Most Medicare supplement plans will cover the deductibles and coinsurance associated with Medicare Part A and even provide an additional 365 days of coverage in a hospital or medical facility setting.

What Does Medicare Part A Cost?

For most, Medicare Part A will not cost anything in retirement. This would be the case if you worked at least 40 quarters (10 years) in the United States and paid Medicare taxes while employed. You may also be eligible for coverage if you didn’t work or pay Medicare taxes but your spouse did.

What Does Medicare Part B Cover?

Medicare Part B is health insurance that covers outpatient medical services that are deemed either medically necessary or preventive. Medically necessary services are “services or supplies that are needed to diagnose or treat your medical condition.” Preventive services are services performed to prevent or detect illnesses.

Medicare Part B benefits include:

Ambulance service

Inpatient and outpatient care

Clinical research

DME (Durable Medical Equipment)

Medicare Part B has a deductible of $257 (in 2025) that is owed prior to receiving benefits. This will be paid directly to the medical provider and not to Medicare. Medicare will record these personally paid medical expenses as reported by your physician and will know when your deductible has been met.

After the deductible is met, you’ll pay 20% for most medical services. There is no cap on what you might pay out-of-pocket. It can get expensive if major medical services are needed.

You may also be subject to up to an additional 15% in excess charges if allowed in your state and a physician decides to charge the additional fee. This is exceedingly rare but you should always check with your physician’s billing person or department to understand if they charge the extra 15% excess charge.

You can search whether a medical service is covered by Medicare by visiting the following page: www.medicare.gov/coverage.

What Does Medicare Part B Cost?

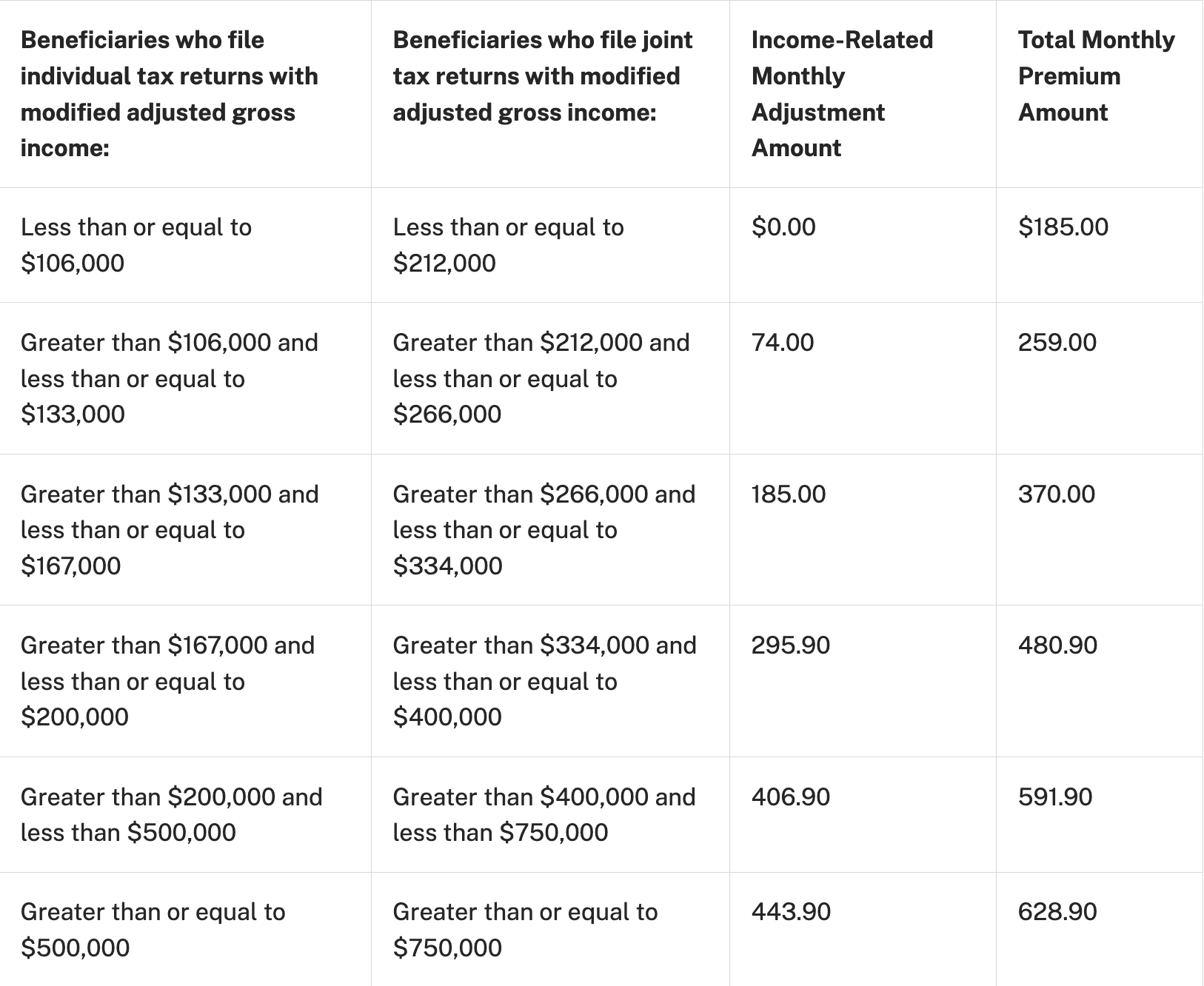

This can get a little confusing as there are multiple factors considered to determine what your Medicare Part B premium is, including when your Part B start date is and your income level.

The short answer is the standard Medicare Part B premium is $185 per month in 2025. However, that’s not what all beneficiaries pay. There are three categories of beneficiaries paying different premiums. Take a look at the chart below:

What is the Medicare Part B Penalty?

In most cases, if you don’t sign up for Part B when you’re first eligible, you’ll have to pay a late enrollment penalty. You’ll have to pay this penalty for as long as you have Part B. Your monthly premium for Part B may go up 10% for each full 12-month period that you could have had Part B but didn’t sign up for it. Also, you may have to wait until the General Enrollment Period (from January 1 to March 31) to enroll in Part B. Coverage will start July 1 of that year.

Usually, you don’t pay a late enrollment penalty if you meet certain conditions that allow you to sign up for Part B during a Special Enrollment Period.

Bottom line here is – don’t make the mistake of not enrolling in Medicare Part B when you are first eligible. Yes, it is elective coverage. However, the penalty will apply if you take Part B after the Initial Enrollment Period or a Special Enrollment Period.

Read more about enrollment periods here: Medicare Enrollment Periods.

If you have questions regarding Medicare eligibility or enrollment periods, please call medigapHelper: (480) 508-4112

What Services Do Medicare Parts A & B Not Cover?

Medicare doesn’t cover everything. If you need certain services that Medicare doesn’t cover, you’ll have to pay for them yourself unless you have other insurance.

If Medicare covers a service or item, you generally must pay your deductible, coinsurance, and copayments, unless you have a Medicare supplement that covers them.

Some of the items and services that Medicare doesn’t cover include:

Long-term care (AKA custodial care)

Most dental care*

Eye exams related to eye glasses*

Dentures*

Cosmetic surgery

Acupuncture

Hearing aids and exams*

Routine foot care

*Ask medigapHelper about a Dental, Vision, & Hearing Plan (DVH plan) to cover these services

Why Buy a Medicare Supplement?

As you have come to understand by reading the information above, Medicare will cover most of your medical services at Medicare providers. Your exposure will be a deductible for Medicare Part A, a deductible for Part B, possible 15% excess charges (though rare nowadays); however, your biggest threat is the 20% coinsurance you’ll be responsible for on medical expenses after you meet your Part A and Part B deductibles.

In the case of a major medical event, you could owe tens of thousands of dollars in medical expenses if you don’t have a Medicare supplement plan to help cover those costs for you.

A Medicare supplement policy is a private insurance plan that helps to cover such things as the Medicare Part A deductible, Medicare Part B deductible, 20% coinsurance, and excess charges.

Medicare supplement plans are completely standardized by Medicare and are offered as plan letters with each plan offering different coverage for the different areas of exposure.

FOLLOW THE LINK BELOW TO COMPARE MEDIGAP PLANS:

Medicare Supplement Plan Comparison Chart

How to Decide Which Medicare Supplement to Buy?

As discussed earlier in this guide, Medicare supplement plans are completely standardized. This is a big part of the “secret sauce” to making the right decision on which Medicare supplement plan to buy and which company to buy it from.

The 3 main areas of standardization include:

Same Benefits – Simply put, if you get a Plan F from one company, it’ll have the exact same benefits as a Plan F from any other company. The same is true of any other plan. A company cannot offer more or fewer benefits for the same standardized plan offered by another company. This sure makes shopping a whole lot easier.

Same Doctor’s Network – Because Medicare supplement insurance is a supplement to traditional Medicare, each supplement plan from every company has access to the entire Medicare network of doctors. There is not a Medicare supplement plan available from any company that provides a larger network of doctors. It’s completely standardized. You don’t have to ask your doctor if they take your Medicare supplement company or plan. You must only ask if they take Medicare.

Same Claims-Paying Process – Claims-processing is automated and simplified for every plan from every company. When your physician files a claim, it goes to a 3rd party intermediary company. This company is notified by the insurance company when you have a Medicare supplement. So, they know which plan and company you have. The intermediary files the claim for Medicare and, once approved by Medicare, they file the claim with your Medicare supplement insurance company. Ultimately, your doctor receives their payment from Medicare and separately receives the balance due (based on your plan benefits) from the Medicare supplement insurance company. The only thing you had to do was show your Medicare ID, and possibly your Medicare supplement ID, to your physician, receive your medical services and leave. The whole claims-paying process is handled automatically. This works the same for every plan from every company.

After reading about the level of standardization in these plans, you should realize that shopping for the right Medicare supplement plan is a matter of determining which plan you prefer and which company it makes sense to buy it from – much of it based on who is offering the lowest rate for the preferred plan.

Your decision may also include brand familiarity and A.M. Best rating, which is a letter grade indicating the financial strength of the insurance company. Any company that has a B+ rating or better is considered financially stable.

Contact medigapHelper at (480) 508-4112 to review plans and rates and A.M. Best ratings from the top providers and even some good companies you might not be as familiar with. Within a few minutes, you should be able to determine which plan and company makes most sense for you.

Will I Get Rate Increases Every Year?

Unfortunately, it’s almost certain that you will. Medicare supplement insurance is a type of health insurance, and health insurance costs tend to go up by single-digit percentages each year. Trying to predict if, and by how much, a particular plan from a particular company will go up from year-to-year is arguably more difficult than trying to guess how a stock will perform in the next year.

Because of this, medigapHelper provides an extended free service for clients, called RATEWATCH that proactively monitors your rate increases versus other offerings and alerts if another offering has a better value. This is a service you will typically not find from other Medicare supplement agencies and is something our clients tell us they greatly appreciate.

What About Medicare Part D?

You can also easily find the best Medicare Part D plan for your current medications (if any). These Part D plans are not completely standardized. However, Medicare’s Prescription Drug Plan Finder tool allows you to enter in your current medications and determine which Part D plan is accepted by your preferred pharmacy and can save you the most money.

How Can I Cover Dental, Vision & Hearing Services Not Covered by Medicare?

medigapHelper has researched several options and has determined that, in our opinion, a combined Dental, Vision, and Hearing (DVH) plan makes the most sense. It combines the deductible for all three services. So, any covered expense for any of the three services is applied to the deductible. We researched the available DVH plans and found the offering that provides the most value.

Ask medigapHelper for coverage and pricing information on this DVH policy.